Blank 4 Point Inspection Form

Key takeaways

When filling out and using the 4 Point Inspection form, several key considerations can help ensure accuracy and compliance. Here are five important takeaways:

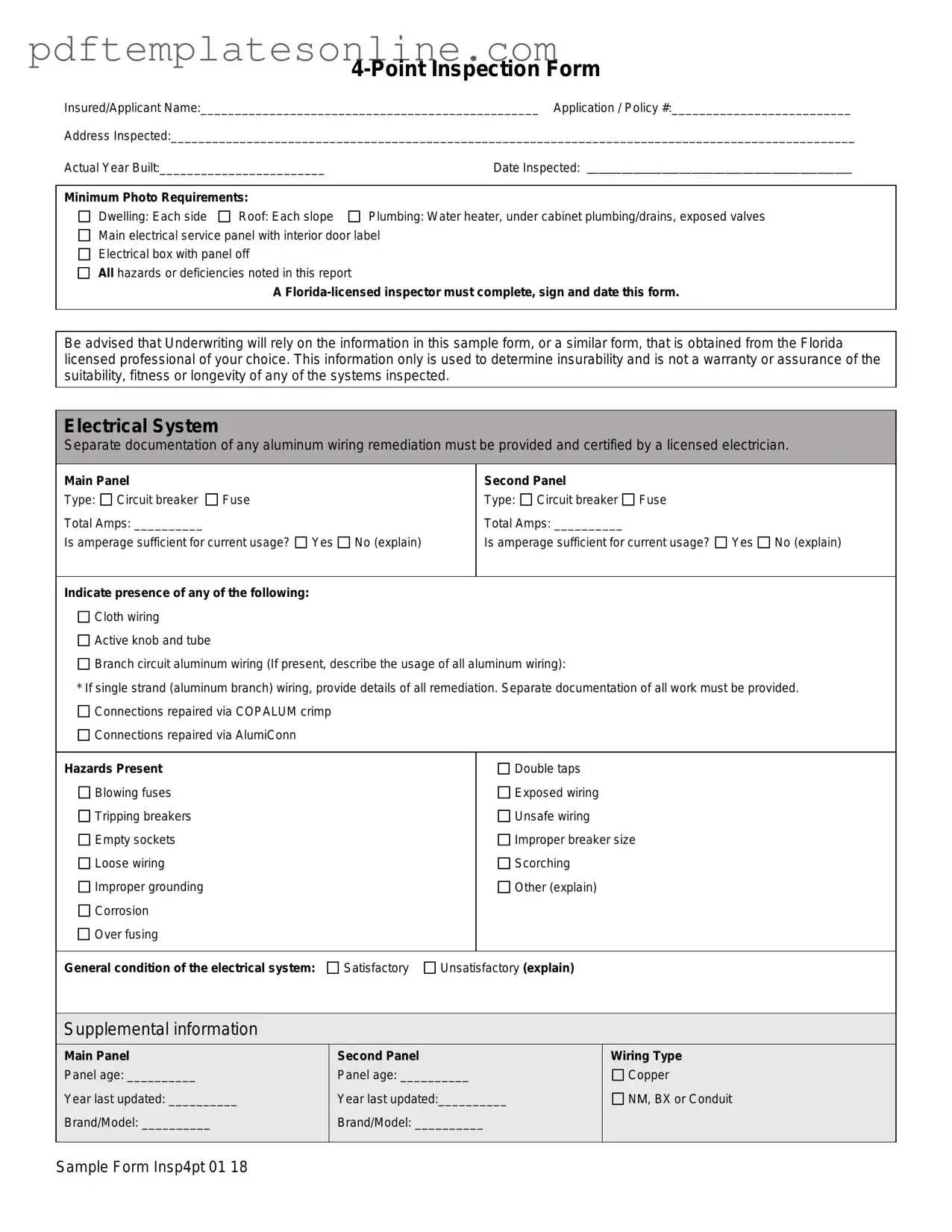

- Complete Information is Essential: All sections of the form must be filled out thoroughly. This includes the insured's name, policy number, and details about the property being inspected. Missing information can delay processing or result in rejection.

- Photo Documentation: Adhering to the minimum photo requirements is crucial. Each side of the dwelling, all slopes of the roof, and key plumbing and electrical components must be documented with clear photographs. This visual evidence supports the written findings of the inspection.

- Licensed Professionals Only: The inspection must be conducted by a Florida-licensed inspector. Their signature and license number are required on the form to validate the inspection. Using an unlicensed inspector can lead to complications in the underwriting process.

- Detail Any Hazards: If any hazards or deficiencies are identified during the inspection, they must be clearly noted. This includes issues with the electrical system, HVAC, plumbing, or roof. Providing detailed explanations helps underwriters assess the insurability of the property accurately.

- Review Before Submission: It is the responsibility of the agent to review the completed form before submitting it with an insurance application. Ensuring that all requirements are met can prevent delays and ensure the application is processed smoothly.

Common mistakes

Completing the 4 Point Inspection form accurately is crucial for obtaining insurance coverage. One common mistake is failing to provide the insured/applicant name and application/policy number. These identifiers are essential for linking the inspection report to the correct insurance application. Without this information, the report may not be processed, leading to delays or denials.

Another frequent error involves the actual year built of the property. Some individuals either guess or provide an incorrect year, which can affect underwriting decisions. It is vital to verify this information through reliable sources, such as property records, to ensure accuracy.

Inadequate documentation of the minimum photo requirements is also a common oversight. Each side of the dwelling, all roof slopes, and key plumbing and electrical components must be photographed. Missing photos can result in a lack of clarity regarding the property's condition, which may hinder the underwriting process.

Many people overlook the need for a licensed inspector to complete, sign, and date the form. Submitting an unsigned or undated form can invalidate the inspection. Ensure that the inspector is not only licensed but also meets the specific requirements outlined for the 4 Point Inspection.

Another mistake involves neglecting to indicate the presence of hazards in the electrical system. Failing to note issues such as double taps, exposed wiring, or improper grounding can lead to significant safety concerns. It is essential to be thorough and honest about any hazards found during the inspection.

In the HVAC system section, some individuals fail to provide details about the primary heat source or the last servicing date. This information is crucial for assessing the system's reliability. Without it, the inspector may not have a complete picture of the HVAC's condition.

When detailing the plumbing system, individuals sometimes forget to check for active leaks or prior leak indications. This oversight can lead to future problems if existing issues are not reported. Thoroughly inspect all visible plumbing fixtures and connections to appliances to ensure no signs of damage are overlooked.

Lastly, when discussing the roof, many fail to provide a complete assessment of its condition. Noting visible signs of damage or deterioration is essential for a comprehensive evaluation. If there are any concerns, they should be documented in detail to inform the underwriting process accurately.

Misconceptions

Misconceptions about the 4 Point Inspection form can lead to confusion and misunderstandings. Here are ten common misconceptions, clarified for your understanding:

- It guarantees insurance approval. The 4 Point Inspection form is not a guarantee of insurability. It provides information to assess risk but does not ensure coverage.

- Only the roof is inspected. The form covers four critical systems: the roof, electrical, HVAC, and plumbing. All must be evaluated.

- Any licensed inspector can complete the form. Only a Florida-licensed inspector can sign off on the form. This ensures the inspection meets state standards.

- It replaces a full home inspection. The 4 Point Inspection is not a substitute for a comprehensive home inspection. It focuses on specific systems only.

- Photos are optional. Photos are required for each section of the inspection. They serve as visual evidence of the condition of the systems inspected.

- All systems must be in perfect condition. While satisfactory conditions are ideal, the form allows for some deficiencies as long as they are documented.

- Aluminum wiring is always a deal-breaker. While it raises concerns, aluminum wiring can be acceptable if properly documented and remediated.

- The inspector's opinion is final. Inspectors provide their assessment, but underwriters ultimately make the decision on insurability.

- Only recent updates matter. The form requires documentation of all updates, regardless of when they occurred, to provide a complete picture.

- It’s only for older homes. Any home, regardless of age, may require a 4 Point Inspection when applying for insurance.

Dos and Don'ts

Do:

- Ensure the form is filled out completely with accurate information.

- Provide clear and detailed descriptions of any hazards or deficiencies.

- Attach all required photos for each section of the inspection.

- Have a Florida-licensed inspector complete, sign, and date the form.

- Document the condition of each system thoroughly.

- Review the form for any missing information before submission.

- Include supplemental information where necessary, especially for repairs or updates.

Don't:

- Leave any sections of the form blank or incomplete.

- Submit the form without the required photos.

- Use a non-licensed inspector to complete the form.

- Neglect to explain any deficiencies noted during the inspection.

- Provide vague or unclear descriptions of issues.

- Submit the form without ensuring all rules and requirements are met.

- Assume that verbal communication suffices; always document everything in writing.

Other PDF Forms

Written Estimate for Auto Repair - Fill out this form to understand potential expenses for car repairs.

Understanding the implications of a California Non-compete Agreement form is essential for both parties involved. While such agreements are primarily intended to protect businesses from potential competition, their enforceability in California is limited. Employers and employees alike should familiarize themselves with the nuances of these agreements, which may lead them to resources such as California PDF Forms for further guidance on navigating these legal documents effectively.

30-day Eviction Notice California - It establishes a clear end date for the tenancy agreement.

Detailed Guide for Writing 4 Point Inspection

Completing the 4 Point Inspection form is an essential step in assessing the condition of a property. After filling out this form, it will be submitted to the appropriate parties for review. Ensure all sections are accurately completed to avoid delays in processing.

- Fill in the Insured/Applicant Name: Write the full name of the insured or applicant at the top of the form.

- Enter Application/Policy Number: Include the relevant application or policy number next to the name.

- Provide the Address Inspected: Clearly write the complete address of the property being inspected.

- Indicate the Actual Year Built: Note the year the property was constructed.

- Record the Date Inspected: Write the date when the inspection took place.

- Gather Minimum Photos: Take photos of the dwelling (each side), roof (each slope), plumbing (water heater, under cabinet plumbing/drains, exposed valves), and the main electrical service panel with the interior door label.

- Complete the Electrical System Section: Document details about the main panel and second panel, including type, total amps, and any hazards present.

- Assess the HVAC System: Indicate whether there is central AC and heating, and if the systems are in good working order. Provide the date of the last servicing.

- Fill in the Plumbing System Section: Answer questions about leaks, water heater location, and the condition of plumbing fixtures. Include the age and type of piping.

- Evaluate the Roof: Describe the roof covering material, age, and overall condition. Document any visible signs of damage or leaks.

- Add Additional Comments/Observations: Use this section for any further details or observations that may be relevant.

- Sign and Date the Form: The Florida-licensed inspector must complete, sign, and date the form to certify its accuracy.